Mike Consedine, EVP and Global Head of Government and Regulatory Affairs at Athene: Regulators care about two things: market solvency and consumer protection.

Mike Downing, Co-President of Athene USA & Chief Operating Officer of Athene Holding: As a fellow Mike, I’ll open it with you.

Mike Consedine: Thank you.

Mike Downing: I think you've got a really interesting perspective on the regulatory front. You've got a pretty remarkable resume: former Commissioner and former NAIC CEO. What are your, kind of, observations of Athene—against, how we operate against the backdrop of your long-term history as a regulator?

Mike Consedine: Well, I mean, one of the things I've always been passionate about in the insurance sector is what it does for society and what it does for the policyholders. You know, being there for people when they really need you the most is really the mission of Athene and the mission of the insurance sector.

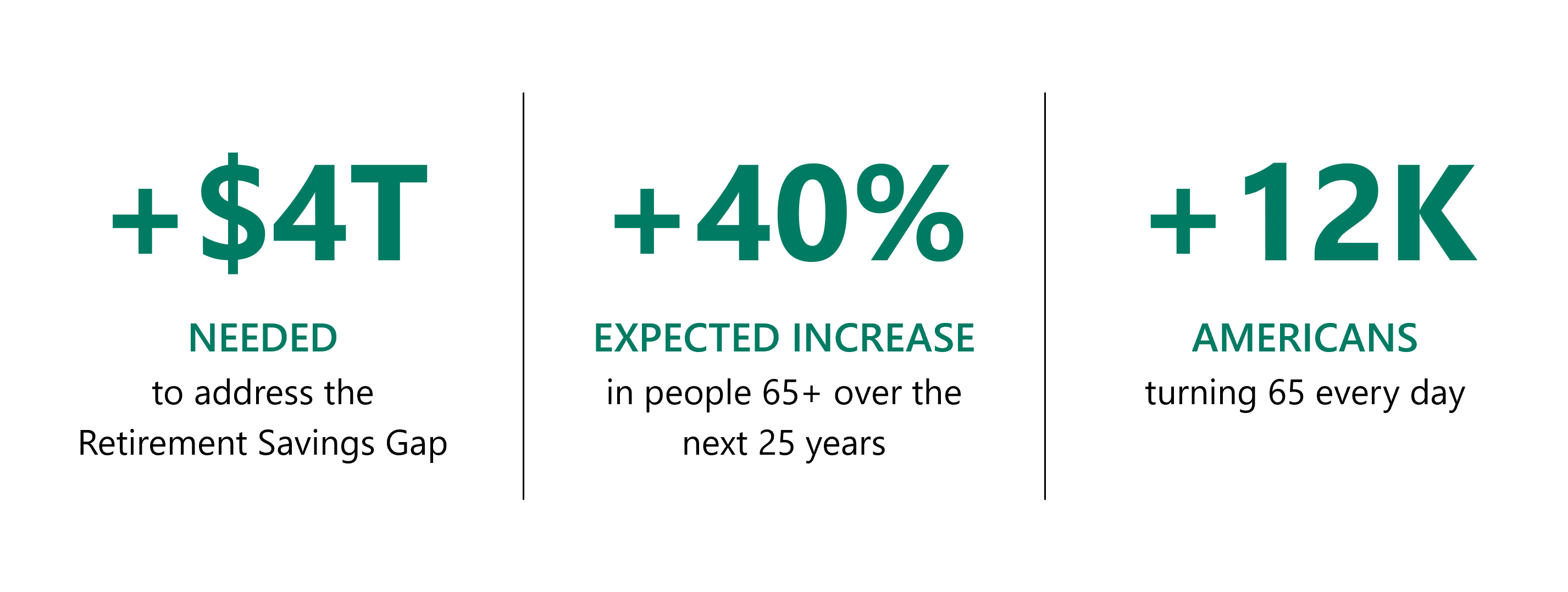

Mike Consedine: And, you know, as a regulator, I had a deep appreciation for the companies that were really true to that mission, true to their policyholders. We have this huge retirement crisis, right, going on in this country right now. And we need the private sector solutions and we're part of that. So that's a pretty cool thing for us.

Mike Downing: There's the federal system and the state system. Insurance has been well steeped in the state. What are some of the differences and why would we think the state system is actually better in some respects?

Mike Consedine: We are very unique, right? In terms of globally having a state-based system. You look across the world, most of the countries have a single regulator. We have 50 states. So 50 regulators, plus the territories. And that's worked for us. And I think it's worked for us for a couple of reasons. One, you know, you look at the size of U.S. markets. You’ve got four of the largest markets in the world are U.S. states. Insurance is personal. And it's really important to have your insurance regulators where the risk exists, in the communities.

John Golden, Partner, Global Head of Financial Regulation at Apollo: These are their constituents. If you look at the, if you look at the strength of the system, it's not only about touching the consumer, it's about the safety of the system. The system has been around for a long, long time. This has a huge track record. Long, long track record of fundamental safety towards the consumer. We're providing long-term savings, providing long-term promises, guarantees. The regulators are very close to the consumer thinking about the construct of the system around that particular type of promise.

Mike Consedine: Yeah, I mean, you're in Iowa. I mean, you're right there in the community with our regulator. It's a great relationship to have when the regulators are right there with the companies, right there with the consumers, you know, and regulate to that market.

Mike Downing: So there’s 50 regulators.

Mike Consedine: Yep.

Mike Downing: How do they all work together?

Mike Consedine: That used to be my former job as CEO of the NAIC. And a lot of people really don't understand, A: Our state-based system or what the NAIC is. They think it's a regulatory, or government agency. Or they think it's a trade association. It's a little bit of everything. But at the end of the day, it's really the connective tissue that ensures coordination between those 50 states, plus the territories. And it does it through strong accreditation practices. So every state is accredited, which is really important safeguard to ensure that they're all meeting similar standards in terms of solvency.

Mike Consedine: The NAIC is also a standard-setting organization. So they'll create model laws and regulations, which then go out to the states to adopt. That helps with uniformity and consistency, as much as possible, across the states. The states talk to each other. You know, they challenge each other. They debate each other. It's a really fascinating organization to be part of. As a former regulator from Pennsylvania, I had 50 plus of my colleagues looking over my shoulder, checking my math. And yeah, that got annoying at times, but it also made sure you were doing your job and making sure that the system as a whole was credible and safeguarded.

Mike Downing: So talk a bit about, Mike, about this state-based system versus the federal system and why you've been a longtime advocate of the values of a state-based system.

Mike Consedine: Yeah, I'm a big proponent of our state-based system, because first and foremost, it's closer to the policyholders. You have regulators in the communities where the policyholders and companies are. They're very invested both in the outcomes and financial solvency of the companies. They're very invested in protecting the policyholders.

John Golden: Yeah, absolutely. I would also add that they're coordinating with the federal government quite extensively as well. So they coordinate with the Federal Reserve. They coordinate with Treasury. There's a non-voting member of the NAIC on FSOC. [On] the international level, they coordinate through the IAIS for cross-border issues, and they are involved in the FSB and so forth. So from the standpoint of them being on an island, that's by no means the case. And I think one of the elements of regulation today is that there's more coordination across all types of financial sectors than ever before.

Mike Downing: Right, so you almost have three levels of collaboration.

John Golden: Absolutely.

Mike Downing: There’s been a lot of innovation. And Athene has been a driver, together with Apollo, a lot of the innovation in the insurance industry. How have you seen the regulatory environment, whether it's Iowa or on a more national level, kind of adapt to some of the innovation and react to it and get ahead of it?

John Golden: Yeah look, I would start with the founding of Athene. I mean, when we came into the market there were a lot of structural issues in the whole financial sector. And we were seeing insurance industry essentially return capital right before it really needed to raise a lot of capital as to help serve the retirement gap and guarantee income. And the regulators saw that phenomenon. So they went to work and said, okay, well, this is a bit of a question of not what is, but what should be. And they were able to listen to us and really understand that the system needed to change. Markets were becoming more private. Public markets were becoming more concentrated. So there needed to be more availability of credit products to support the annuity and retirement products that consumers needed. So rather than chasing that away, they dug in and said, hey, how do we do this responsibly?

Mike Consedine: I mean, at the end of the day, regulators care about two things: market solvency and consumer protection. Innovation is important, but you really have to solve for the first two. So Athene to its credit, presents innovation in the context of we can make sure that the markets are stable, companies are solvent. We can make sure consumers are protected and we can present innovation that really solves for the retirement gap. And so I think we've gotten to a place where they don't necessarily see innovation, itself, as a risk. They see innovation as a part of the evolution of the system, which is a great place for us to be.I think an area of innovation has simply been the level of transparency that we put together, where we're leading. Often we don't get a lot of followers, but how’s that example of us being a leader in transparency—

John Golden: I kind of go back to the beginning of our formation and thinking about what our philosophy is around the regulators—and Marc and Jim Belardi— [it] was very clear that we needed to be what I’ll call rigorously transparent. Not just meeting the four corners of the rules and basically telling them what they needed to know, but going above and beyond and explaining why things are happening, what's happening in the market, what are people doing that's good and bad—helping them think through regulatory policy. And I kind of think about what would have happened had firms like ours not been that way. I don't know that we'd be here. I don't know that the industry would be as powerful as it is today if we didn't have that disposition. And so that is foundational to our philosophy. You know, when we speak with peers, we advocate for this, what I call rigorous transparency, all the time.

Mike Consedine: To John's point, but for particularly, you know, what Athene and Apollo have done in terms of not just engagement and transparency, but real thought leadership, the market would not be where it is today, at least with the perspective of, of the regulators, which has now shifted to really embracing sort of this approach and the benefits that it can have for the market and for consumers. So much so that we now see a lot of other more traditional companies replicating that structure.

Mike Downing: And one of the things I've seen in terms of the regulatory, observation kind of from my chair in the regulatory environment, is how well they've done to really go back to first principles.

John Golden: That's a testament to the NAIC. One thing that's very, very clear is that they do have a north star of trying to achieve intellectual consistency across risk.

Mike Consedine: We're grateful that regulators don't regulate by virtue of hot takes. They regulate based on actual analysis, understanding of the market, thorough data collection. You know, our regulators know Athene and Apollo inside and out because we are fully transparent, not only to them but publicly. For us, showing our math is not a problem. It's actually what gives credibility to Athene and Apollo and to the greater system.

John Golden: The stable regulatory environment and positive, strong relationships with regulators doesn't raise capital. It doesn't solve the retirement gap. But it's a necessary condition to that outcome. The regulators really understand that. And are actually working alongside of us to ensure a stable and safe system that achieves that goal.

Mike Downing: Thanks for putting it in context.

Mike Consedine: Well, thanks for letting us nerd out a bit on insurance regulation.

John Golden: Our pleasure. Thank you. Thanks, Mike.