America is facing a widely recognized retirement crisis.

Although retirement solutions providers have made important—and consistent—strides toward mitigating risks for retirees (from portfolio diversification to investment biases to longevity risk), key concerns remain.

Despite $34 trillion in retirement assets, Americans face a staggering $3.7 trillion shortfall in meeting projected retirement needs.1 This gap is fueled by longer lifespans, portfolios ill-equipped to deliver durable income over decades and insufficient returns.

Along with the savings gap, Americans’ defined contribution portfolios—401(k), 403(b), 457(b) plans and more—face a number of hurdles and are missing a potential opportunity to increase returns, enhance diversification, reduce volatility risk, protect principal and secure income.

Here are four charts illustrating the challenge.

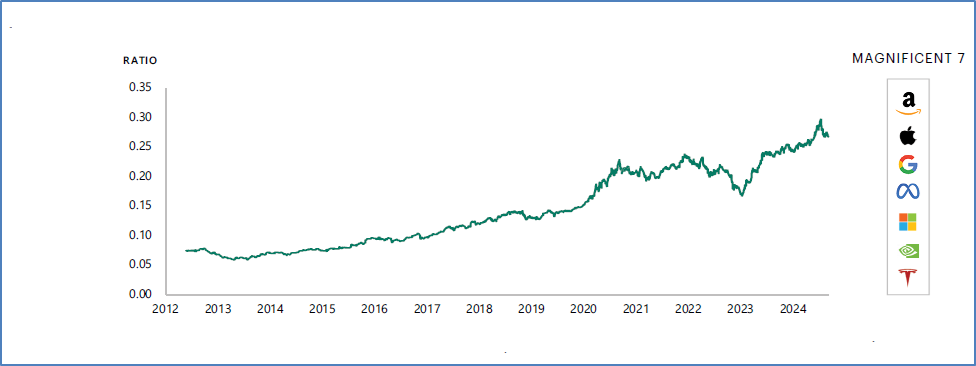

1. The Public Equity Market Has Become Highly Concentrated

Ratio of Magnificent 7 market cap to Russell 3000 market cap

Data as of August 2024. Company names and logos are trademarks of their respective holders. Sources: Bloomberg, Apollo Chief Economist

As of 2022, global defined benefit plans had 23% of their assets invested in private markets, with that number jumping to 32% and 39% among endowment and family offices, respectively.2 Defined contribution portfolios, however, had near zero exposure to private investments. They’re almost 100% allocated to public markets that are highly concentrated. As of August 2024, just seven companies—Apple, Amazon, Meta, Alphabet, Microsoft, Nvidia, and Tesla—represent 27% of the entire Russell 3000’s market cap. This concentration not only raises portfolio risk but weakens diversification, making public equity markets increasingly fragile and volatile on their own.

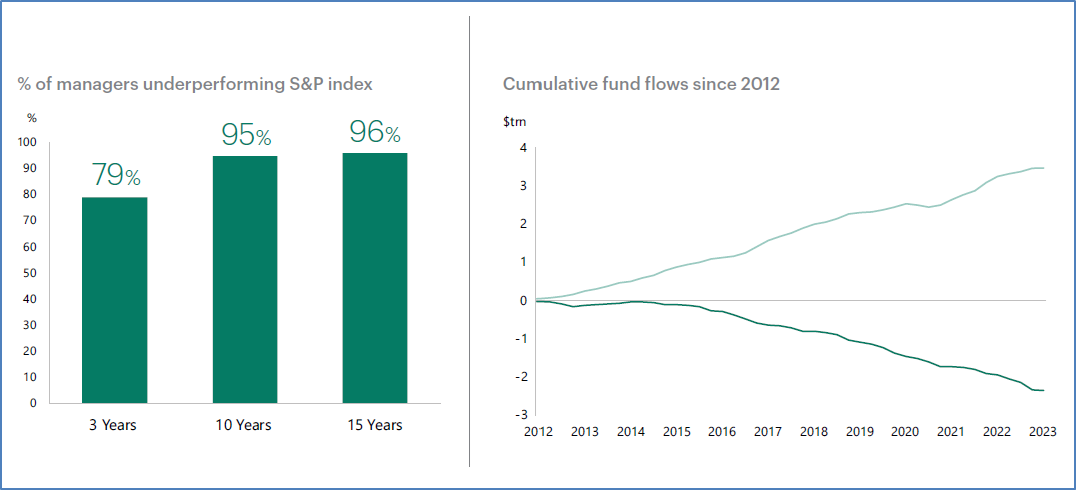

2 & 3. Public Markets Now Deliver Beta, Not Alpha

Public equity markets have become beta...

Leading to a wholesale rotation from active to passive strategies

Source: S&P Global SPIVA US Scorecard 2023

Data as of December 31, 2023. Sources: Bloomberg, Apollo Chief Economist

Active managers are losing the benchmark battle. Over a 15-year span, a staggering 96% of active equity funds underperformed the S&P 500. In response, capital has flooded into passive vehicles, exacerbating market concentration and correlation. For investors, this means fewer opportunities to outperform—and more exposure to systemic risks.

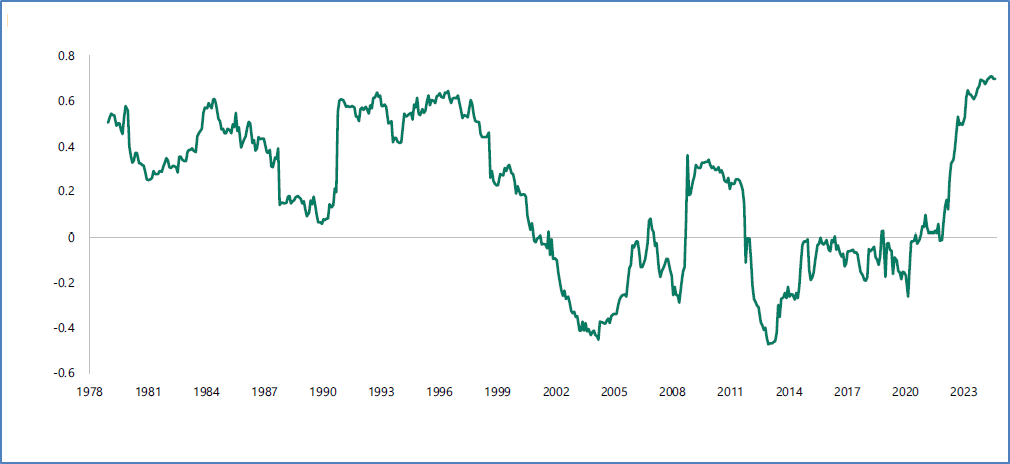

4. The 60/40 Portfolio Has Lost Its Diversification Edge

Rolling three-year correlations between stocks and bonds

Data as of August 2024. Sources: Bloomberg, Apollo Chief Economist

Traditionally, the 60/40 stock-bond portfolio offered a reliable buffer against volatility. But as interest rates rose and stock-bond correlations increased, the diversification benefits have eroded.3 This chart shows how, since 2021, bonds no longer provide the offsetting force they once did—just when retirees need stability most.

The Bottom Line

The message from the data is clear: America’s retirement portfolios aren’t meeting their potential. Public market-only strategies are not enough to close the funding gap, navigate volatility, achieve greater diversification, or generate sustainable income.

Rethinking retirement means incorporating new tools such as private markets and guaranteed income, to build more resilient, diversified and outcome-oriented portfolios—before it’s too late.

- Cerulli for estimated retirement assets, as of November 2022; Jack VanDerhei, Ph.D., “Impact of Various Legislative Proposals and Industry Innovations on Retirement Income Adequacy,” ebri.org, January 20, 2021, for estimated funding gap

- Defined Contribution Institutional Investment Association: “Alternative Investments in Defined Contribution Plans,” February 2022.

- Matt O’Mara, “How alternatives can address your 60/40 portfolio blues,” Apollo Global Management, July 2022.

Tags

The information contained in this commentary is provided for educational and informational purposes only and should not be construed as financial or investment advice, nor should any information in this commentary be relied on when making an investment decision.

Opinions expressed herein reflect the current opinions of Apollo Analysts as of the date appearing in this commentary only. This commentary is not complete and the information contained herein may change at any time without notice. Apollo has not made any representation or warranty, expressed or implied, with respect to fairness, correctness, accuracy, reasonableness, or completeness of any of the information contained herein (including but not limited to information obtained from third parties unrelated to Apollo), and expressly disclaims any responsibility or liability therefore.

This commentary does not constitute an offer of any service or product of Apollo. It is not an invitation by or on behalf of Apollo to any person to buy or sell any security or to adopt any investment strategy, and shall not form the basis of, nor may it accompany nor form part of, any right or contract to buy or sell any security or to adopt any investment strategy. Nothing herein should be taken as investment advice or a recommendation to enter into any transaction.

Past performance is not necessarily indicative of future results.

Please click here for additional important disclosure information.